Incurred Cost Submissions: A Government Contractor's Complete Guide

Learn how to prepare and submit incurred cost submissions (ICS) for government contracts. Covers FAR 52.216-7, DCAA ICE model, deadlines, penalties, and tips.

Tiatun T.

Federal Sales Consultant · Apr 8, 2026

This article explains incurred cost submissions (ICS) — what they are, who must file them, what goes inside them, when they are due, and what happens if you get them wrong. By the end, you will understand the full lifecycle of an ICS: from the Federal Acquisition Regulation (FAR) clauses that trigger the requirement, through the schedules and reconciliations that make up the submission, to the final rate negotiation that closes out your contracts. Whether you are a first-time government contractor trying to understand how to win government contracts on a cost-reimbursement basis, or a seasoned business development director looking for the penalty thresholds and quick-closeout nuances you may have overlooked, this guide is written for you.

What This Article Covers — and Why It Matters

The incurred cost submission is one of the most consequential administrative requirements in government contracting — and one of the most frequently misunderstood. Miss it and you may forfeit cost recovery you legitimately earned. Get the numbers wrong and you face penalties that can dwarf the original error. Handle it well and you close contracts cleanly, free up cash flow, and build a track record of financial credibility that supports future bids. This guide walks through every element, from the FAR trigger clause through the rate negotiation that ends the cycle.

What Is an Incurred Cost Submission?

An incurred cost submission — sometimes called the “final indirect cost rate proposal” or “incurred cost proposal (ICP)” — is an annual filing in which a government contractor proposes its final indirect cost rates for a completed fiscal year. Think of indirect costs as the shared expenses that support all of your projects but cannot be charged to any single contract: things like rent, utilities, your accounting staff’s salaries, and company-wide software licenses. These costs get grouped into pools (such as fringe benefits, overhead, and general & administrative (G&A) expense) and then spread across contracts using an allocation base (such as total direct labor dollars or total cost input). The ICS is where you formally tell the government, “Here are the rates I actually experienced this year, here is the math, and here is how those rates affected each of my flexibly priced contracts.” [1]

The submission serves three essential purposes. First, it reconciles what you billed during the year — using estimated provisional billing rates (PBRs) set under FAR 42.704 — against your actual costs [2]. Second, it gives the government’s auditors and contracting officers the data they need to verify that every dollar you claimed was allowable (permitted under the FAR Part 31 cost principles), allocable (properly assigned to the right cost objective), and reasonable (what a prudent business person would pay) [6]. Third, once final rates are negotiated under FAR 42.705, both sides “true up” — you either refund money to the government or receive additional payment — and the contract can be closed out [2].

Who Must Submit — and When

You must file an ICS if you hold any flexibly priced federal contract or subcontract that includes the clause FAR 52.216-7, Allowable Cost and Payment [1]. “Flexibly priced” is the FAR’s umbrella term for contract types where the government reimburses actual costs rather than paying a fixed price. The most common examples are cost-reimbursement contracts (cost-plus-fixed-fee, cost-plus-incentive-fee, cost-plus-award-fee), but the requirement can also apply to the cost-reimbursed portions of time-and-materials (T&M) and labor-hour (LH) contracts when FAR 52.216-7 is incorporated. The key action item: check each contract’s clause set. If 52.216-7 is in there, you have an ICS obligation.

The filing deadline is straightforward: within six months after the end of your fiscal year [1]. If your fiscal year ends December 31, the ICS is due by June 30. If it ends September 30 (matching the federal fiscal year), you must submit by March 31. The Contracting Officer (CO) — specifically, the Administrative Contracting Officer (ACO) who oversees your indirect rates — can grant a written extension, but you must request it before the deadline passes. Do not assume silence is consent; get the extension in writing.

What happens if you miss the deadline or submit something that does not meet the adequacy requirements? The ACO has the authority to unilaterally establish your final indirect cost rates under FAR 42.705(c) [2]. “Unilaterally” means without your agreement. These government-imposed rates tend to be conservative — lower than what you would propose — and can significantly reduce your cost recovery. In a competitive landscape where understanding how to win government contracts often hinges on accurate cost management, losing recoveries to a preventable administrative failure is an unforced error.

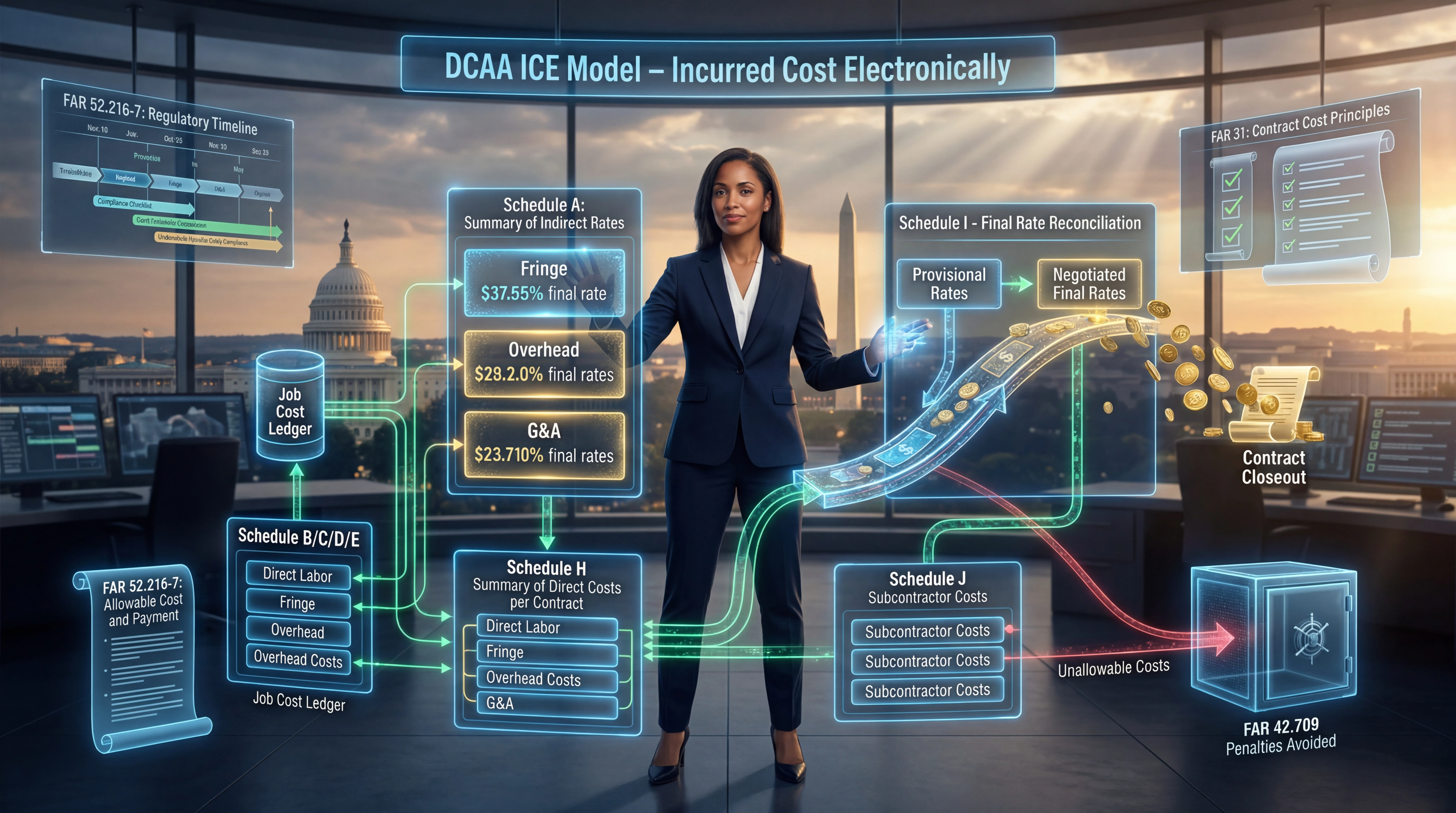

What Goes Inside the Submission

FAR 52.216-7(d)(2)(iii) specifies the minimum content for an adequate ICS [1]. In practice, however, the Defense Contract Audit Agency (DCAA) has established the de facto standard through two tools: the DCAA Incurred Cost Electronically (ICE) model — a set of pre-formatted Excel schedules — and the DCAA Incurred Cost Submission Adequacy Checklist, which auditors use to screen your filing before they even begin a substantive review [8]. Even if your cognizant audit agency is not DCAA (some civilian-agency contractors are audited by other organizations), using the ICE model and passing the adequacy checklist is the safest approach.

The following table summarizes the core schedules and what each one does:

| Schedule | Common Name | What It Shows |

|---|---|---|

| Schedule A | Summary of Rates | Your proposed final indirect cost rate for each pool (fringe, overhead, G&A, etc.) and the allocation base used. |

| Schedules B–E | Indirect Pool Detail | The individual cost elements (account-level detail) that make up each indirect pool, so auditors can trace every dollar. |

| Schedule F | Allocation Base Detail | The composition of each allocation base — for instance, every direct cost element included in “total cost input” for your G&A rate calculation. |

| Schedule H | Contract Cost Ledger | Total direct costs incurred on each contract and subcontract during the year, tied to your general ledger. This is the schedule auditors scrutinize most heavily. |

| Schedule I | Cumulative Allowable Cost Worksheet (CACWS) | For each flexibly priced contract, the cumulative allowable cost from inception through the fiscal year, compared with cumulative billings. This is where the true-up happens. |

| Schedule J | Subcontract / Intercompany Costs | Detail of subcontractor and affiliated-entity costs, which the government reviews for reasonableness and proper flow-down of audit requirements. |

| Schedule K | Reconciliation Schedules | Books-to-claimed reconciliation, labor reconciliation (timekeeping to payroll to job cost), and identification of unallowable costs removed from the pools. |

Alongside these schedules, you must include the Certification of Final Indirect Costs required by FAR 52.242-4 [5]. This certification must be signed by an individual with authority to bind the company — typically a senior officer — and it states, under penalty of law, that the indirect costs included in the submission are allowable under the contract terms and applicable cost principles. This is not a formality. The certification creates personal and corporate accountability.

The Labor Reconciliation: Where Most Problems Start

Experienced practitioners know that the labor reconciliation is both the most important and the most error-prone element of the ICS. Here is why: labor costs typically drive multiple schedules simultaneously. Your timekeeping system records hours by project; your payroll system records dollars by employee; your job-cost ledger records charges by contract. These three data sources must agree. When they do not — and discrepancies of even a few thousand dollars are common in growing companies — the ripple effect touches your direct cost totals (Schedule H), your indirect pool compositions (if labor is misclassified between direct and indirect), and your allocation bases. Reconcile labor first. Lock down the timekeeping-to-payroll-to-job-cost tie-out before you touch anything else in the ICE model.

Unallowable Costs and the Penalty Regime

One of the most critical aspects of learning how to win government contracts — and keep them profitable — is understanding unallowable costs. FAR Part 31 contains dozens of cost principles, each addressing a specific category of expense [6]. Some costs are expressly unallowable, meaning the FAR states in plain terms that they cannot be charged to government contracts. Common examples include:

- Entertainment costs (FAR 31.205-14)

- Alcoholic beverages (FAR 31.205-51)

- Bad debts (FAR 31.205-3)

- Most advertising and public relations costs (FAR 31.205-1, with narrow exceptions for recruitment advertising and certain other categories)

If expressly unallowable costs end up in your ICS — even accidentally — you face penalties under FAR 42.709 [4]. The baseline penalty is equal to the disallowed amount. If the government determines you knowingly included the unallowable cost, or if it is a repeat finding from a prior year, the penalty can increase to two times the disallowed amount. Add to that the original disallowance itself, and you could be paying three times the cost in total. These penalties are assessed per occurrence, and they accumulate quickly.

The defense against this risk is structural. Maintain a clearly labeled unallowable cost account in your chart of accounts. Every expense that is expressly unallowable should be coded to this account at the time of booking — not scrubbed out months later during ICS preparation. Document your screening procedures in writing, train your accounts payable staff, and review the unallowable account during monthly close to confirm it is catching what it should. When you build the ICE model, the unallowable amounts should already be segregated and should flow into the reconciliation schedules (Schedule K) as identified adjustments.

From Submission to Final Rates: What Happens Next

After you submit the ICS, the cognizant audit agency (typically DCAA for Department of Defense (DoD) contractors) reviews it against the adequacy checklist [8]. If the submission passes, the auditors schedule a substantive audit — though backlogs mean this can take months or even years. During the audit, DCAA examines your claimed costs for allowability, allocability, and reasonableness, and issues an audit report with findings and a recommended set of final rates.

The ACO then uses the audit report as a starting point for rate negotiations under FAR 42.705 [2]. You have the opportunity to respond to audit findings, provide additional documentation, and negotiate. Once both sides agree, you sign a rate agreement, and the final rates are applied to all flexibly priced contracts for that fiscal year. The difference between what you billed at provisional rates and what is owed at final rates results in either a refund to the government or an additional payment to you.

For practitioners managing portfolios of contracts, this true-up process has real cash-flow implications. If your provisional billing rates were set lower than actuals, you have been under-billing and will receive money back. If provisional rates were too high, you will owe the government a refund. Smart contractors work with their ACO to adjust PBRs annually so the gap stays small.

Quick-Closeout: A Practical Shortcut

Not every contract needs to wait for final rates. FAR 42.708 provides quick-closeout procedures that allow the ACO to negotiate final indirect cost rates on individual contracts before the full ICS audit is complete [3]. The conditions are that the unsettled indirect costs are relatively insignificant and that quick-closeout is in the government’s interest. This is particularly useful for small task orders or contracts that represent a tiny fraction of your total volume. If you have contracts lingering in “physically complete” status, ask your ACO whether quick-closeout is an option. Closing contracts sooner frees up administrative capacity on both sides and can accelerate final payments. Understanding how to win government contracts also means knowing when and how to close them efficiently.

Subcontractor Considerations

If you are a prime contractor with subcontractors who hold cost-reimbursement subcontracts containing FAR 52.216-7, those subcontractors must submit their own incurred cost submissions. Your ICS cannot be fully resolved until theirs are, because their final indirect rates affect the costs flowing up to you. Validate early that your subcontractors have submitted their ICS or have provided you with their final rates. Primes remain responsible for the reasonableness of billed subcontract costs, and DCAA will ask about subcontractor rate status during your audit.

If you are a subcontractor, everything in this article applies to you. The fact that your contract is with a prime rather than directly with the government does not exempt you from the ICS requirement when FAR 52.216-7 is in your subcontract. Your cognizant agency may be DCAA or another auditor depending on your contract mix and volume, but the submission content and deadlines are the same.

Practitioner Checklist: Preparing a Clean ICS

The following checklist distills the process into actionable steps. Use it alongside the DCAA adequacy checklist as your internal quality assurance gate [8].

- 1 Freeze year-end financials. Close your books and lock the general ledger for the fiscal year before you begin building the ICE model. Any post-close adjustments should be documented and traceable.

- 2 Reconcile labor first. Tie timekeeping records to payroll to the job-cost ledger. Resolve every variance before moving on.

- 3 Confirm allocation base integrity. Verify that your allocation bases (total cost input, value-added, direct labor dollars, etc.) align with your disclosed practices or your Cost Accounting Standards (CAS) Disclosure Statement, if applicable.

- 4 Segregate unallowable costs. Review your unallowable account for completeness. Cross-reference against the FAR 31.205 cost principles to ensure nothing was missed.

- 5 Build the ICE model. Populate each schedule methodically. Cross-check totals between schedules — they must tie.

- 6 Prepare Schedule I (CACWS) for every flexibly priced contract. Confirm cumulative billings and costs from inception, not just the current year.

- 7 Verify subcontractor ICS status. Contact each subcontractor holding FAR 52.216-7 to confirm submission status or obtain final rates.

- 8 Run the DCAA adequacy checklist. Treat it as a final pre-flight check. Every “no” answer is a potential adequacy rejection.

- 9 Obtain the certification signature. The Certification of Final Indirect Costs (FAR 52.242-4) must be signed by someone with binding authority [5].

- 10 Submit on time. If you need an extension, request it in writing from the ACO before the six-month deadline.

- 11 Archive workpapers. Retain all supporting documentation for at least three years after final payment on each contract, as required by FAR Subpart 4.7 [7].

Cost Accounting Standards: A Brief Note

Contractors subject to Cost Accounting Standards (CAS) — generally those with CAS-covered contracts above certain dollar thresholds — must ensure their ICS is consistent with their CAS Disclosure Statement. Inconsistencies between your disclosed cost accounting practices and what appears in the ICS will trigger audit findings and potentially require cost adjustments. If you have recently changed an accounting practice (for example, shifting your G&A allocation base from total cost input to value-added), make sure the change was properly disclosed and that the ICS reflects the transition correctly. For contractors newer to the federal market who want to understand how to win government contracts while staying compliant, CAS can feel overwhelming, but the fundamental principle is consistency: do what you say you do.

Records Retention

Under FAR Subpart 4.7, contractors must retain financial records, cost or pricing data, and supporting documentation for generally three years after final payment on each applicable contract [7]. For ICS purposes, this means your workpapers, general ledger detail, timesheets, payroll records, allocation calculations, and subcontractor correspondence must all be preserved and accessible. If a DCAA audit occurs three years after your submission (not unusual given backlogs), you need to produce the support. A central, well-organized ICS workpaper file — whether electronic or physical — pays dividends during audits and closeouts.

What to Do Next

If you have a flexibly priced government contract and have never filed an incurred cost submission, start by downloading the DCAA ICE model and the adequacy checklist from the DCAA website — both are free. Walk through the checklist line by line against your current accounting setup to identify gaps. If your fiscal year end is approaching, begin your labor reconciliation now; it is the single step most likely to delay your submission if left until the last minute. And if you are a newcomer still exploring how to win government contracts, know that mastering the ICS process is not optional for cost-reimbursement work — it is the price of admission.

Glossary of Terms Used in This Article

ACO (Administrative Contracting Officer) — The government official responsible for administering a contract after award, including overseeing indirect cost rates, billing rates, and contract closeout.

Allocation Base — The denominator used to calculate an indirect cost rate. Common bases include total direct labor dollars, total cost input, or value-added cost input.

Allowable Cost — A cost that meets all four tests under FAR Part 31: it must be reasonable, allocable, in conformance with CAS or generally accepted accounting principles, and not specifically prohibited by the contract terms or cost principles.

CACWS (Cumulative Allowable Cost Worksheet) — Schedule I of the ICE model. It tracks total allowable costs and billings on each flexibly priced contract from inception through the fiscal year to calculate any over- or under-billing.

CAS (Cost Accounting Standards) — A set of 19 federal standards governing how contractors measure, assign, and allocate costs to government contracts. Applicability depends on contract type and dollar thresholds.

CO (Contracting Officer) — The government official with authority to enter into, administer, or terminate contracts and make related determinations and findings.

Cost-Reimbursement Contract — A contract type where the government pays the contractor’s allowable incurred costs, up to a ceiling, plus a fee. The contractor bears less cost risk than under a fixed-price contract.

DCAA (Defense Contract Audit Agency) — The Department of Defense agency that audits defense contractor costs, including incurred cost submissions, to protect the government’s financial interests.

DoD (Department of Defense) — The federal department responsible for military and national security matters. DoD is the largest buyer of contracted goods and services in the US government.

FAR (Federal Acquisition Regulation) — The primary set of rules governing how the federal government purchases goods and services. It covers everything from contract types to cost principles to closeout procedures.

Flexibly Priced Contract — Any contract where the final price is not fixed at award and depends on actual costs incurred. Includes cost-reimbursement, T&M, and LH contracts.

G&A (General and Administrative) Expense — Indirect costs related to the overall management and administration of the business, such as executive salaries, legal fees, and accounting staff costs. G&A is typically the broadest indirect cost pool.

ICE Model (Incurred Cost Electronically) — A standardized set of Excel spreadsheet templates created by DCAA for contractors to use when preparing their incurred cost submission.

ICS (Incurred Cost Submission) — The annual filing in which a contractor proposes its final indirect cost rates and reconciles claimed costs to its accounting records. Also called the incurred cost proposal (ICP) or final indirect cost rate proposal.

Indirect Cost Pool — A grouping of indirect costs that share a common allocation base. Typical pools include fringe benefits, overhead, and G&A expense.

LH (Labor-Hour) Contract — A contract type similar to T&M but without a materials component. The government pays fixed hourly rates for labor.

PBR (Provisional Billing Rate) — An estimated indirect cost rate set by the ACO that contractors use for interim billing purposes until final rates are negotiated.

Quick-Closeout — A procedure under FAR 42.708 that allows contracts to be closed before final indirect rates are established, when the unsettled costs are relatively insignificant.

T&M (Time-and-Materials) Contract — A contract type where the government pays fixed hourly labor rates plus actual material costs. It is used when the scope of work is too uncertain for a fixed-price contract.

True-Up — The financial adjustment made after final indirect rates are established, reconciling the difference between what was billed at provisional rates and what is owed at final rates.

Unallowable Cost — A cost that may not be charged to a government contract. “Expressly unallowable” means the FAR specifically names the cost as unallowable in direct terms.

References

[1] FAR 52.216-7, Allowable Cost and Payment. Federal Acquisition Regulation, Acquisition.gov.

[2] FAR Subpart 42.7, Indirect Cost Rates (including FAR 42.704, Billing Rates, and FAR 42.705, Final Indirect Cost Rates). Federal Acquisition Regulation, Acquisition.gov.

[3] FAR 42.708, Quick-Closeout Procedure. Federal Acquisition Regulation, Acquisition.gov.

[4] FAR 42.709, Penalties for Unallowable Costs (including FAR 42.709-1). Federal Acquisition Regulation, Acquisition.gov.

[5] FAR 52.242-4, Certification of Final Indirect Costs. Federal Acquisition Regulation, Acquisition.gov.

[6] FAR Part 31, Contract Cost Principles and Procedures (including Subpart 31.205, Selected Costs). Federal Acquisition Regulation, Acquisition.gov.

[7] FAR Subpart 4.7, Contractor Records Retention (including FAR 4.705). Federal Acquisition Regulation, Acquisition.gov.

[8] DCAA Incurred Cost Electronically (ICE) Model and Incurred Cost Submission Adequacy Checklist. Defense Contract Audit Agency.